Issue #17: The Long Tail

This is our last week in Boise, ID and we could not have had a better time. While we did not try the famous potatoes (french fries don’t count), we did our fair share of eating and exploring. I can write with conviction that we will definitely be back.

Our topic this week was inspired by a recent discussion with @HelloShreyas, who if you aren’t following, you should be.

In 2004, Chris Anderson, then the CEO of Wired Magazine, wrote an article called the “The Long Tail” popularizing the theory that the Internet’s natural economies of scale allow companies to profitably sell niche products with low volumes (the long tail), where before, they were only focused on selling large quantities of the most popular products (the head).

For decades, companies were limited to selling products that had broad appeal because there were inherent constraints and fixed costs, mainly that distribution and inventory was expensive. Retail stores only have so much shelf space, so they stock products they know most people will buy. Radio stations only have so much air time and survive on ads, so they need to prioritize the most popular songs to maximize the number of listeners. Theaters have physical space constraints and prioritize movies they know will attract the most people. They want the biggest bang for their buck, and who can blame them.

The Internet changed that dynamic by making it more cost effective to support the long tail. For media in particular, the Internet brought distribution costs down to nearly zero, making it profitable to support niche content. We now have websites dedicated to obscure corners of pop culture, musicians that can sustainably provide music to their 1000 true fans, and e-commerce marketplaces like Amazon supporting the long tail of consumer products.

The bulk of the consumption still happens at the “head", but the Internet and platforms like Spotify, Youtube, Amazon and Substack make it possible to survive in the long tail (and in my case, the veeery end of the long tail).

The same thing is happening with assets.

Let’s zoom in…

Breaking Barriers

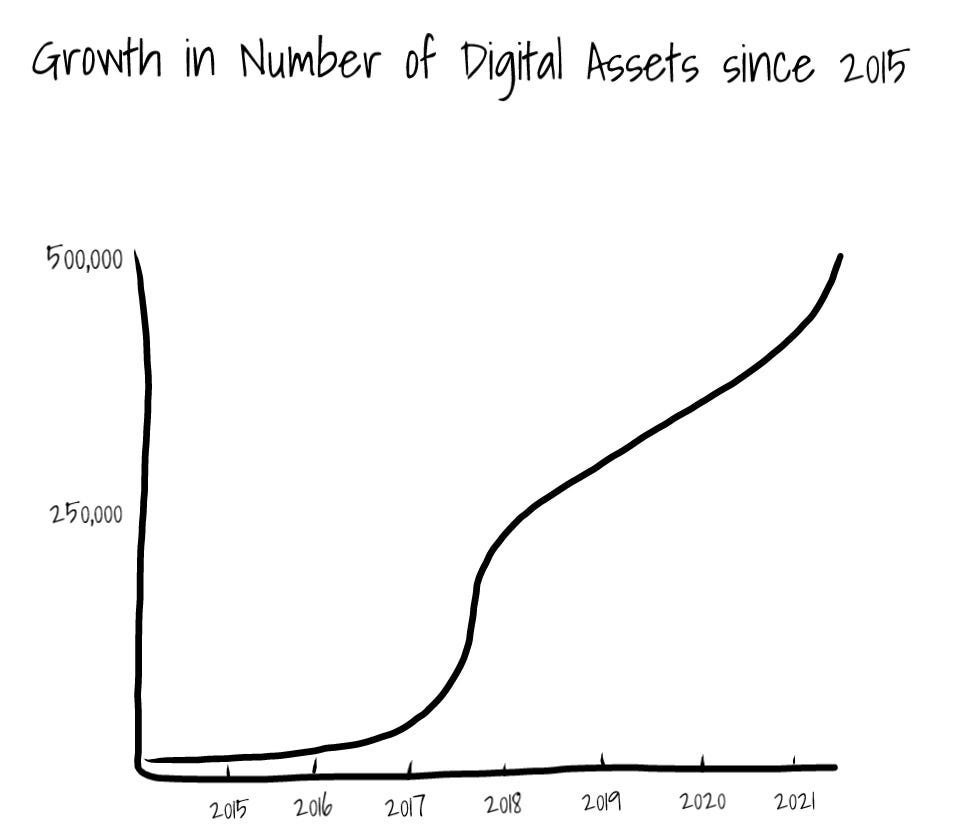

In 2014, there were approximately 300 different digital assets. Many of them were simple clones of Bitcoin. In 2016, that number started to explode and over the course of the next 5 years, the number of digital assets grew to approximately 500,000.

This growth was due to two things:

Multi-asset blockchains. Before Ethereum, every blockchain managed a single digital asset. If you wanted to create a new digital asset, you needed to create a new blockchain (there were a few exceptions like Colored Coins on Bitcoin, but they weren’t scalable solutions). Outside of forking an existing blockchain, building a new blockchain took enormous effort. The barrier to creating new digital assets was high.

The introduction of Ethereum and other multi-asset blockchains meant you could create and manage multiple assets on a single ledger. Sounds simple and intuitive now, but it was revolutionary then. This lowered the technical barrier to creating a new asset.

Token standards. Despite having multi-asset blockchains, there wasn’t a standard way of representing new assets initially. If you wanted to issue a new digital asset you needed to create a brand new smart contract. This wasn’t as technically difficult as creating a new blockchain, but it was still effort.

Eventually, standards were proposed and adopted. We now have widely adopted token standards (aka templates) that lowered the technical barrier to creating a new asset even more.

Today, there are approximately 400,000 different ERC20 contracts on the Ethereum blockchain, that means there are roughly 400,000 different fungible digital assets live on Ethereum. There are another 11,000 ERC721 contracts, which means 11,000 non-fungible digital assets (NFTs) live on Ethereum. Combine these totals with the digital assets on other Layer 1 blockchains and you get close to 500,000.

Now the vast majority of the 500,000 have no value and aren’t widely held. But, I highlight this to demonstrate that the barriers to creating new digital assets are being removed. It’s getting easier and cheaper.

The long tail of assets is forming, and the trend will continue.

Choices

Have you ever thought about the investment opportunities available to you? For most people, there isn’t much variety. You can buy stocks, bonds, index and mutual funds, and real estate. If someone has an investment portfolio, 99% of the time it is made up of these assets.

While the investing experience has changed a lot over the years, the choices haven’t changed much at all. Until recently, my generation and my parent’s generation invested in the same types of assets.

Now consider all the new types of digital assets today: cryptocurrencies (BTC, ETH), governance tokens (UNI, COMP), interest bearing stablecoins (cDAI), liquidity pool tokens (LPs), no-loss lotteries, and the universe of NFTs. If nothing else, the crypto economy has created a ton of choice of retail investors.

And this is just the tip of the iceberg. The low hanging fruit. For the foreseeable future, there will be a Cambrian explosion of new digital assets in almost every industry. The industries most likely to generate the bulk of new assets are finance, gaming (metaverse/virtual reality) and media (social, entertainment, IP).

Let’s look at gaming.

NFTs are being used to represent ownership of in-game items like avatars, clothes and weapons. Because these items live outside their respective games, on blockchains, they now become an asset in the crypto economy. These NFTs can be bought, sold, borrowed against, lent out, even grouped together and securitized. This blurs the lines between virtual reality and the real world, because the assets in each transcend their previous boundaries. Virtual real estate now has a market value outside the game. Rare avatars have a market value outside the game. This adds millions of new digital assets to the pool, and introduces an entirely new vertical of investable asset to the financial markets.

The Long Tail of Financial Markets

Two weeks ago I wrote about the consolidation of financial market infrastructure into a single tech stack (Internet + public blockchains + DeFi protocols). In the context of the long tail of digital assets, another way to think about this is the long tail of financial markets.

In some ways, the existence of a financial market for something is what makes it an asset. If you can’t assign a dollar value to something, and it can’t be part of a financial transaction, is it really an asset?

Since the Internet is becoming global, asset-agnostic financial market infrastructure, it naturally becomes the market infrastructure for the long tail in the same way it is the market infrastructure for the head. It makes more things assets!

This is exciting because it means the creation of hundreds of mini-financial markets for even the more obscure things. Every thing has a market price and can be an input in a financial transaction.

In theory, this should means things are more efficiently priced and transacted, even in the long tail.

Parting Thoughts

If this plays out like I’ve predicted above, everything becomes an investable asset, tradeable in a marketplace with a market price. We are essentially taking the barter economy, and stacking financial market infrastructure on top.

Most people will hold the most common, accessible assets, but there will be a long tail because the cost of creation is low and demand is there.

This will create enormous value for a lot of people, and especially the platforms that enable and capture this activity.

There is a downside to the “financialization” of everything though. We start assigning a dollar value to everything thing, decision and interaction. Since everything has a value, our decisions becoming increasingly based on whether that decision is smart financially.

Just like we’ve lost some of our humanity to smart phones and social media, I worry we will lose more of it when everything is optimized for the best financial outcome.

Thanks for reading,

Andy

--

Not a subscriber? Sign up below to receive a new issue every Sunday.

Andy, join our discord server: https://discord.gg/RKJFJYn7BB

I have been thinking a lot about the state of financial literacy, particularly in the age of DeFi. As you said, the options for investing were relatively limited, particularly for non-accredited investors, for generations. When we teach personal financial planning, at all levels, we inevitably focus on strategies that use these products. Anything that did exist in the long tail seemed to be either unavailable to ordinary people, or too good to be true, but that is changing. At Bloq, we are really big on accessibility and ease of use. I wonder though about how education plays a role, and how it can be done to not only grow the industry, but to level the playing field for those we look to serve. Thanks for sharing this each week!