Issue #8: Ownership

In the last month, we’ve looked at the business models of DeFi protocols and how users and liquidity could scale over time. This week, I want to explore ownership. Will protocol ownership resemble that of the largest financial market utilities, or will it look more like a publicly traded tech company?

I have a hunch, but it’s fun to stumble through my thought process together. This issue is 70% brainstorm, 30% prediction.

Let’s zoom in…

Ownership Distribution

When Facebook went public in 2012, founders and employees owned almost 40% of the company. Early investors like Accel Partners and Peter Thiel owned another 15%. This was after raising $2.3B over half a dozen rounds of funding. The Google cap table looked similar at IPO. Larry and Sergey collectively owned 32%, and other employees together owned 15%.

Cap tables in DeFi look different. Not unrecognizably different, but different.

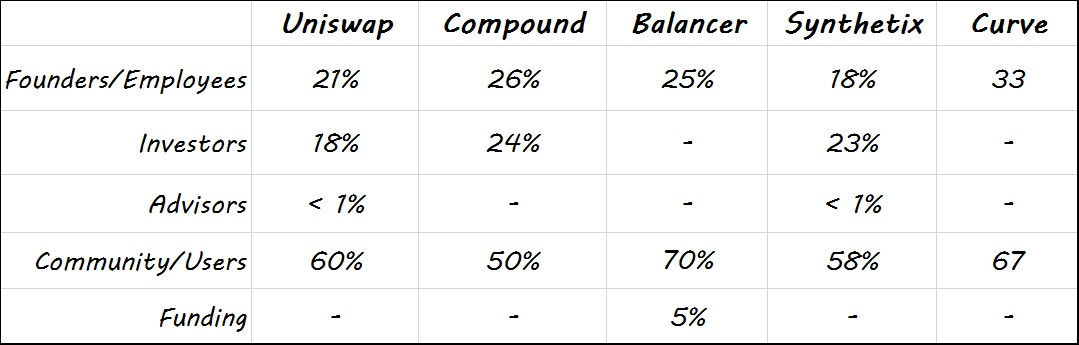

Across the board, founders and employees of DeFi protocols own less of their projects than their counterparts at traditional tech companies. Case and point, the original token distribution for Uniswap:

Founders & Employees – 21%

Investors – 18%

Advisors - <1%

Community – 60%

The Uniswap team, including the founders, hold 21% of the total supply of UNI. The same is true at most of the major protocols. On average, founders and employees collectively hold between 20-30% of the token supply, typically locked and vested over a 4-year period.

The lower percentage is due to the fact that a majority of tokens are earmarked for the community and/or users. Companies that took outside money, either from VCs or an ICO, allocated between 50-60% of the token supply to their communities and users. A few are even higher in the case of Balancer (70%) and Curve (67%).

Will large community and user distributions impact what protocol ownership looks like in a decade?

Maybe. Read on…

Institutions…welcome to the party!

As the narratives around DeFi evolve and more institutional investors wake up to the fact that protocols could become trillion dollar businesses, expect more institutional investment products to hit the market. The most recent example of this is Bitwise. On February 17, Bitwise announced a new DeFi index fund recently with significant positions in Uniswap, Aave, Synthetix, Maker and Compound among others.

More funds will follow.

This is a similar trend that played out with large tech companies after they went public. Hedge funds, mutual funds and other asset managers buy up large blocks of the stock, either on their own behalf or as agent for their clients. This has a concentrating effect over time.

VCs Cashing Out?

Venture funds like a16z, Polychain, Paradigm and Pantera currently own large blocks of protocol tokens as a result of their early investment in the companies. Eventually, they need to deliver returns to their investors.

In your average tech company IPO, VCs will typically sell a portion of stock in the public offering. After a mandatory 6-month lock up, remaining shares can be sold or transferred directly to the LPs in the fund to lock in profits and collect the carry.

Will the same process playout in Defi? It could…

Funds holding protocol tokens are under the same pressure to return profits to their investors, the only difference is they are holding tokens instead of stock. While the tokens are easy to sell on the open market, they may not be as easy to distribute to LPs. A pension fund or family office likely doesn’t have the same ability to take possession of tokens the same way they would shares.

Given the complexity of receiving and managing tokens though, one possibility is the lifespan of the funds are extended to serve as a de facto custodian for LPs tokens.

SIFMUs

I’ve described DeFi protocols as public financial infrastructure, and I think this is an accurate description given they are now part of the broader fabric of the Internet. In traditional finance, there is a term for critical infrastructure – Systemically Important Financial Market Utilities, or SIFMUs.

Terrible acronym aside, SIFMUs include organizations like the DTCC, the central securities depository in the US that maintains a record of every publicly traded security in circulation, and CHIPS, the real-time multilateral payment system typically used for large dollar payments ($3M+).

Unlike public companies, SIFMUs are owned by their users – the large commercial and custody banks that hold and process the majority of funds and transactions, respectively. The ownership model makes sense in this context because these organizations are operating infrastructure for the sole and direct purpose of serving these institutions.

Will DeFi protocol cap tables resemble SIFMUs and consist of the largest institutional users (exchanges, custodians, etc.)?

Not likely. While I still view DeFi protocols as public utilities, how they came into being was very different than SIFMUs. They began as startups, many of which had founding teams and took venture money. As a result, their ownership has resembled a startup and will track the startup path.

Where do we end up?

My hunch…

Protocol ownership in 10 years looks similar to big tech ownership today.

Founding teams will continue to maintain large token positions, but as I discussed above they will be smaller than the equity positions of public tech company founders because 50-60% of tokens on average are committed to the community. It’s also reasonable to assume founders will sell a portion of their position once vesting and lockups expire. These markets are highly liquid.

The remaining tokens will be held by outside investors, either institutions or individuals.

Will large asset managers like Fidelity, Blackrock and others own protocol tokens on behalf of their end clients?

Yes. University endowments, pension funds and sovereign wealth funds will eventually pile money into DeFi the same way they’ve piled money into FANG stocks over the last decade, and into Bitcoin over the last year. And they will do so through their traditional agents…the large asset managers.

Parting Thoughts

Here’s a breakdown of Amazon’s stock ownership as of October 2020 for additional context.

Thanks for reading,

Andy

Not a subscriber? Sign up below to receive a new issue every Sunday!

Thanks for writing this =)