Issue #63: The End of Idle Assets

People and businesses need resources. We need cars to get from A to B. We need homes for shelter and sleep. We need money to pay for necessities.

But we don’t need access to these things all the time. The average person spends one hour behind the wheel each day. Our cars sit idle in driveways, parking garages and on streets the other 23 hours. You don’t need that guest room to host friends and family year round. The room is empty most of the time.

Sharing economy platforms like Uber, Turo and Airbnb created global marketplaces that connected the unmet demand with underutilized supply.

Financial markets and services work the same way. We don’t need access to every dollar, bond and share of stock we own all the time, and intermediaries are there to match the unmet demand with underutilized supply.

The same market has been built around crypto assets.

Assets shouldn’t, and won’t, sit idle.

Let’s zoom in…

No Idle Assets

Let’s assume you have $15 in your pocket. There is value to having cash on hand. You have the ability to use it at your discretion. However, like the car in your driveway, you aren’t using the money constantly throughout the day. You don’t actually need the cash until the moment the merchant says “your total today comes to $15”. Up until that point, your cash is an underutilized asset.

If you were optimizing for utility, you would put it into your checking account. When you’re not using it, a bank will use it to finance credit cards, mortgages, small business loans and lines of credit. Then the moment you swipe your debit card at the store, the $15 will be there.

Prior to 2018, crypto assets were like cash in the sense they sat idle in wallets. There was nothing to do with them. It was a very capital inefficient market and a CFO’s nightmare.

The emergence of proof of stake blockchains, lending platforms and DeFi created instant utility for crypto assets. Stake them to the secure the network. Lend them to a borrower. Provide trading liquidity to a decentralized exchange. The only difference is there is no bank in the middle facilitating the activity to maximize earning potential and minimize risk. It’s on you to find the demand and maximize the utility.

Just like Uber and Airbnb did for drivers and empty rooms respectively, staking platforms and DeFi apps made it easier to maximize asset utility by connecting underutilized crypto assets with unmet demand.

Now how do you measure/compare utility value? Utility is priced in the form of staking rewards, interest rates and trading fees. Whoever or whatever values that asset the most will pay more to use it.

Today, the only justification for not putting your crypto assets “to work” for you is (a) the need for instant liquidity, or (b) concern over the security/technology risk (a real concern too, because hacks are frequent).

Compounding Utility

Crypto has something that traditional forms of money, cars and guest rooms don’t have - standard formats and programability.

These features of today’s crypto assets give them an ability to have compounding utility. That means the maximum utility value of an asset can be realized at all times, and the utilized version of that asset has additional utility.

I tweeted this in 2019…

I was envisioning a world where everyone holds and pays for things in “lent dollars”. I’m maximizing the utility of my dollar by lending it out, and I still enjoy the purchasing power it holds.

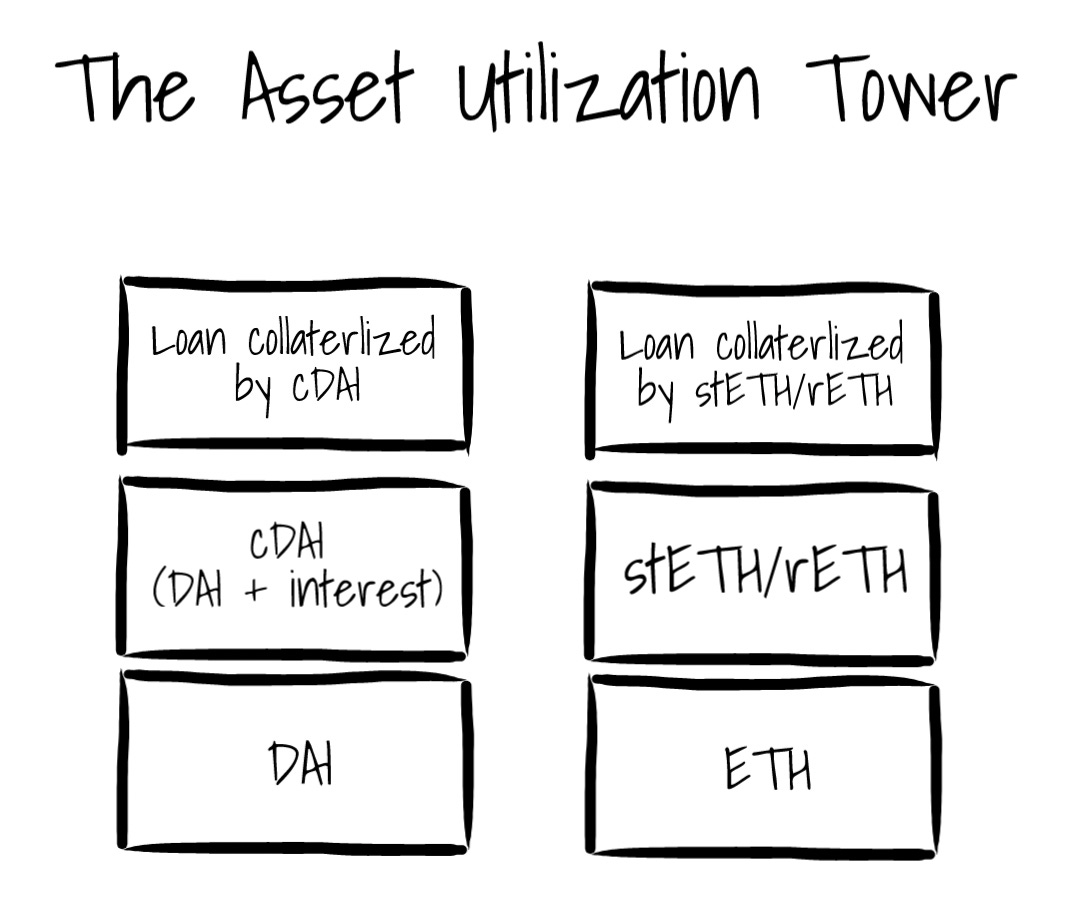

Let’s say you have $1,000 of a stablecoin (ex: DAI). You contribute your 1,000 DAI to a lending pool on Compound, and in return receive an amount of cDAI tokens that serve as your claim on the underlying 1,000 DAI plus the interest those assets generate in the lending pool. DAI is your principal, whereas cDAI is your principal + interest.

The value of these “claims” increases as the underlying asset accrues rewards, interest and fees.

Now aren’t we back to the “claim” assets sitting idle in wallets? Early on, we were. However, a lot of DeFi protocols support the lending and trading of the claim assets too, so they have similar utility.

This means I have the option of holding 100 DAI, or holding 100 cDAI that are accruing interest. Technology risk aside, as long as you can do everything with cDAI that you can do with regular DAI, holding DAI = underutilized asset.

ETH won’t sit idle either.

Staked ETH on Lido (stETH) and Rocketpool (rETH) are the most recent examples of a claim asset with increasing utility. Called “liquid staking”, stETH/rETH are claims on ETH staked with Lido’s and Rocketpool’s ETH 2.0 staking validators + the accrued staking rewards.

Right now, Ethereum has a total circulating supply of ~120M. As of April 8, only 10,833,914 ETH were staked. Roughly 9%. This seems low considering staking rewards are 4.5% annually compared to average borrow rates of less than 2%. But remember, staked ETH is locked until ETH 2.0 launches (expected later this year).

Post launch and lock up, ETH should pour into staking because (a) it offers the highest yields in the market, and (b) the claim assets (stETH/rETH) are liquid.

Samyak is right. stETH/rETH will probably become the preferred collateral in DeFi. The only thing you can’t do with them are pay gas fees.

CDO-squared

I marvel at the financial innovation, but there’s a scene from The Big Short playing in the back of my mind.

During their “research” trip to Florida, Steve Carell’s character has dinner with a CDO manager. The manager is explaining the tower of speculation that exists on top of the residential mortgage market, and walks Carell through the flavors of CDOs (collateralized debt obligations) being sold in the market. When the manager explains that the hottest things in CDO’s are CDO-squared, a CDO of a CDO, and synthetic CDOs (the other side of the CDO bet), Carrel’s character says “that is fucking crazy”, and the manager says “no, it’s fucking awesome”.

Because of token standards and composability, the barrier to creating a new asset or derivative financial product is virtually zero. When you start creating new assets with dependencies on underlying assets, it’s not without risks.

For assets like cDAI, if you ever needed to unwind and redeem the underlying DAI, you are limited by the amount of liquidity in the DAI lending pool. Depending on the size of your position, you might not be able to exit immediately or all at once.

In periods of peak volatility with mass loan/leverage liquidations, things could get interesting.

Parting Thoughts

For certain categories of NFTs (blue chips and assets with in-game utility), similar lending and staking markets are emerging.

We quickly find ourselves in a future where every tokenized asset can find maximum utility.

I’m moving across country next weekend, so the next issue of 30,000 Feet will be in your inbox on April 23. Until then…

Thanks for reading,

Andy

—

Not a subscriber? Sign up below to receive a new issue of 30,000 Feet every Sunday.