Issue #5: Big DeFi Business

From 30,000 Feet

Before I begin, I want to acknowledge that many of the ideas and perspective in this issue came from @lsukernik after a 3-hour conversation a few weeks ago. Larry is a brilliant mind in the industry and deserves credit for explaining to me what I am about to explain to you. The next beer’s on me, Larry.

In previous issues, I’ve described DeFi applications as protocols. But that’s not the entire picture. They are much more than that.

They are products and services generating real revenue, with stakeholders and a governance structure, in many cases with a substantial treasury at their disposal.

They are organizations, albeit more decentralized, and they are going to get really, really big.

I can’t think of a more important topic to explore than how these protocol organizations operate.

Let’s zoom in…

The 101

I want to anchor this exploration in a basic understanding of how organizations operate (apologies to all the MBAs for grossly oversimplifying this):

An organization sells a product or service, and sales generate revenue (income).

The income is used to cover expenses. Anything leftover is distributed to shareholders in the form of dividends, or retained by the organization for future use (retained earnings).

The Finance team manages the organization’s capital and decides how to invest and spend money (treasury management).

Management executes day to day operations of the organization, and reports to a Board of Directors.

The Board of Directors holds Management accountable, and acts in the best interest of the shareholders

Let’s apply this understanding to DeFi protocols…

Revenue

DeFi protocols manage very specific products or services. Some manage collateralized loans, others help you exchange one token for another. Remember, each one is like a financial vending machine living on a blockchain.

In the case of MakerDAO, the protocol acts like a central bank for the Ethereum ecosystem, issuing digital dollars (DAI) to users who deposit collateral. To unlock your collateral, you pay the dollars back plus a fee (akin to an interest payment).

The fees are paid to the protocol, and accrue on the protocol’s internal balance sheet. When accrued fees reach $10,000,000 DAI, they are auctioned off for MKR, the protocol’s governance token. Afterwards, the MKR is burned (aka destroyed), reducing the MKR supply in circulation. This process repeats in perpetuity.

This is similar to an organization using profits to buy back shares from the market. The effect is the same – the supply of MKR tokens and shares in the market goes down, thereby increasing the price of those still outstanding.

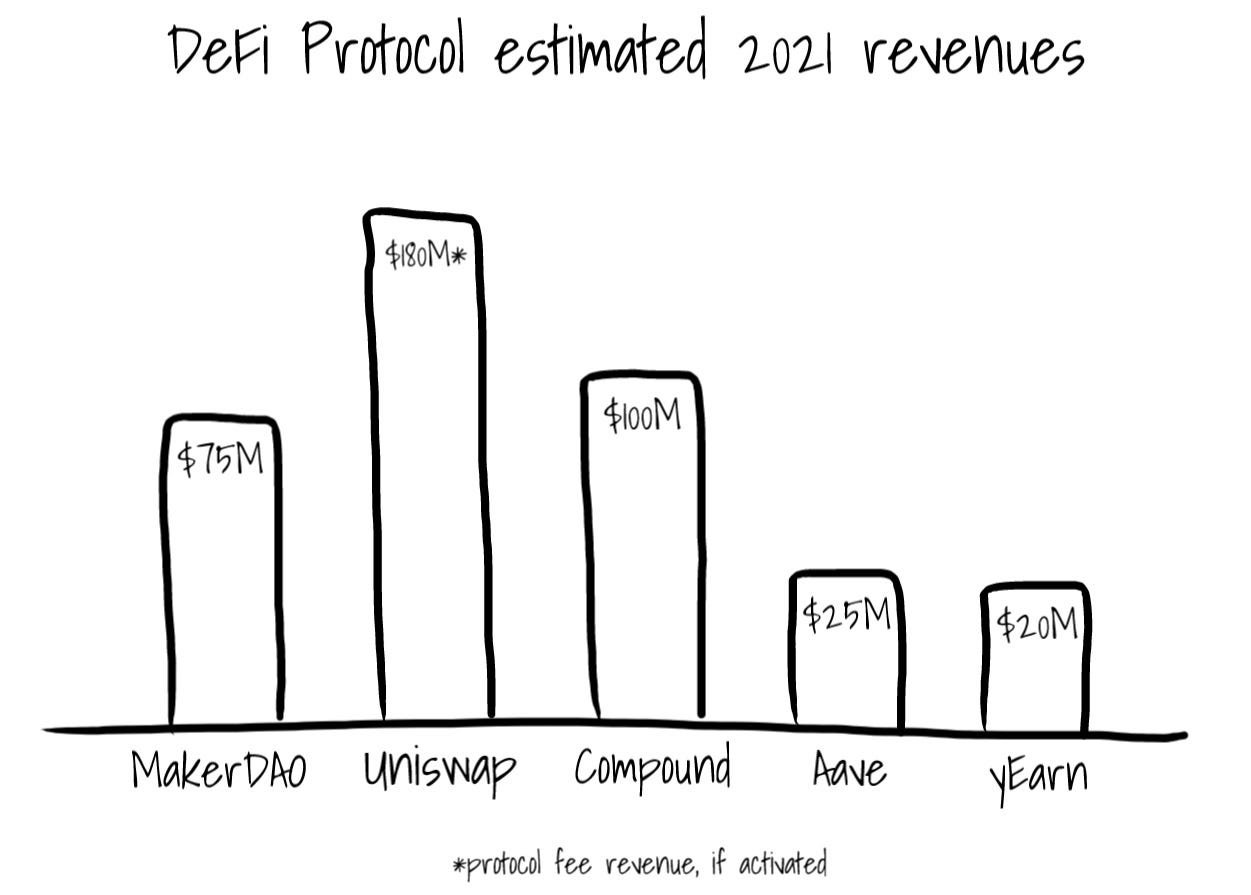

Based on current market activity, MakerDAO is on pace to generate over $75M in fees over the next 12 months. That’s real revenue! And that revenue will get passed on to holders of MKR tokens indirectly via the “burn'“.

Uniswap, the most popular decentralized exchange, has an opportunity to do something similar.

Currently, Uniswap charges a 0.3% liquidity fee on all transactions. The fees immediately go into liquidity reserves and distributed pro rata to Uniswap’s liquidity providers. As of September 2020, Uniswap had generated over $56M in fees for 49,000 liquidity providers.

Interestingly, there is a protocol fee built into the Uniswap protocol, but not active. If turned on, 0.05% of each transaction would accrue to the Uniswap treasury. Assuming current trading volume stayed constant at approximately $1 billion per day, Uniswap would generate $182M in fees over the next 12 months. That’s real revenue! The revenue could be passed on to UNI token holders via a burn similar to MakerDAO, or Uniswap could treat it like retained earnings and use it to support the Uniswap ecosystem.

A third example is Compound, the largest DeFi lending protocol by loan volume. Compound is expected to generate approximately $100M in fees this year, the majority of which are paid out as interest to lenders on the platform.

The fact that these protocols are able to generate tens and hundreds of millions in annual revenues, despite their relative immaturity, should be a signal to everyone, especially Wall Street, that this new financial infrastructure has found both product market fit and a business model.

Dangerous combination.

Treasury Management

Treasury management is how an organization manages capital. Prior to 2017, treasury management was not something startups worried about. But during the heyday of ICOs when crypto projects were raising hundreds of millions of dollars, primarily in cryptocurrency treasury management was suddenly a top priority. Projects like Tezos, whose investment came in the form of BTC and ETH, were very thoughtful, converting a portion of their capital into more stable assets like fiat currencies, commodities and low risk securities like US government bonds.

Treasury management has been a relevant topic in DeFi too, as many of the large protocols are sitting on substantial treasuries consisting primarily of their own governance tokens (ex: Uniswap’s UNI token).

Uniswap’s original treasury consisted of 43% of the total UNI supply (430,000,000 tokens vested over 4 years), valued at almost $13 billion dollars at the time of publishing. This presents an enormous opportunity and responsibility for the Uniswap community to allocate this capital wisely to support the protocol and grow the ecosystem.

Are DeFi treasuries being managed well today? The answer is not really, at least by traditional corporate standards. Generally, the protocol’s token holders vote on how treasury funds are allocated. The challenge with this mechanism is that it is inefficient. Treasury management is a full-time job, and benefits from a clear strategy and centralized decision making. Organizations have short term, medium term and long term capital needs, and a robust treasury management strategy should contemplate all of it.

Protocol teams are realizing this and starting to centralize the decision-making process with grant committees, tasked with reviewing and funding grant requests from the community. Uniswap has also requested proposals for a formal treasury management committee that would develop and execute a strategy for allocating the treasury (I strongly support this move and wish more protocols would do it).

I expect to see more sophisticated treasury management functions and strategies emerge over the next year. These protocols are too critical to the ecosystem, and their treasuries are too large for this not to be a professional function.

Governance

Governance is a term thrown around the industry a lot, and it can be a nebulous thing. Governance.

Generally speaking, governance is overseeing the control and direction of _________. In the corporate sense, governance refers to oversight and control over the direction of a company, and follows a consistent framework:

Company management reports to the Board of Directors

The Board holds management accountable and protects the interests of the shareholders

Shareholders hold the Board accountable

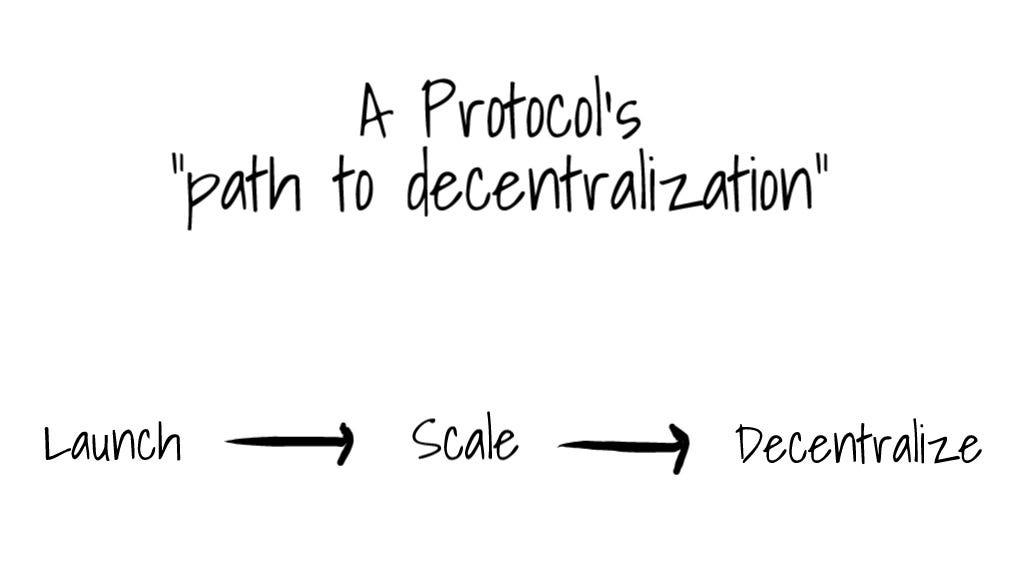

In DeFi, governance refers to oversight and control over the direction of the protocol, but the decisions that need to be made are similar to those at a normal company. For example, deciding to update and expand the product or service, adjusting the fee structure, or setting aside funds for investment. Initially, these decisions are made by the founding team or individual. But for a variety of reasons, including regulatory concerns, governance of DeFi protocols is usually decentralized over time. Practically, this means passing decision-making authority to the holders of the protocol’s governance tokens.

Here’s how it usually happens:

Founding team launches protocol and controls 100% of decision making (necessary to bootstrap growth)

Founding team raises money from investors

Protocol attracts users and liquidity

Founding team decentralizes decision making and distributes governance tokens to team members, investors, users and treasury

Put differently…

Many of the largest DeFi protocols, including MakerDAO, Uniswap, Compound, Aave and Synthetix have either completed or are in the middle of this process. Once the process is complete, a protocol is effectively governed by its token holders.

Now the intention is to decentralize control, but practically what happens is the three-tier corporate governance structure of management, a board of directors and shareholders is collapsed into a single decision-making body, the token holders. And in most cases, the founding team and early investors hold the majority of tokens in circulation. Ironically, many protocols end up being more centrally managed afterwards than they were before. *I’m interested in debating this point, so if you have a different opinion please reach out to me on Twitter @ajbeal*.

I’m actually someone who believes decentralization isn’t always beneficial, and there are good reasons why DeFi protocols aren’t worried about the majority of voting power being held by a few, at least early on. The reality is, a protocol’s “inner circle” is more often than not the most invested in and knowledgeable about the protocol, strategy and future. They should be the ones steering the ship!

Over time, however, distributing control to a broader group of stakeholders ensures that these protocols remain open, public infrastructure.

Final thought

We need to start thinking about DeFi protocols not just as financial applications, but as organizations. How do these organizations evolve to meet the growing demand they will inevitably have to support?

Thanks for reading,

Andy

Not a subscriber? Sign up below to receive a new issue every Sunday!

Where should I wire money in Larry and Andy's fund so I can relax while you both make bank for investors?